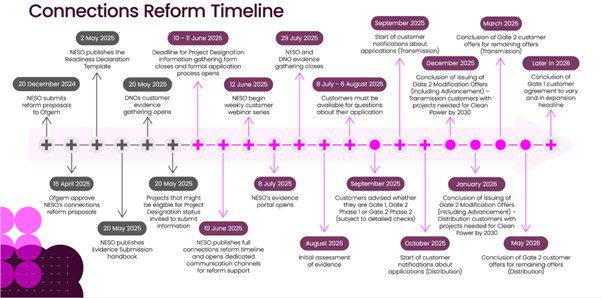

The National Energy System Operator (NESO) grid reforms, centered on the “First Ready, First Connected” (TMO4+) model, mark a radical shift from the legacy “first-come, first-served” queue to a gated system designed to hit the Clean Power 2030 (CP2030) targets. Under this new framework, projects are funneled through Gate 1 (initial application) to Gate 2, which acts as a rigorous “readiness and strategic alignment” filter. To pass Gate 2 and secure a firm connection date, developers must prove they are “shovel-ready” by hitting milestones such as secured land rights and advanced planning permission, while also aligning with the Strategic Spatial Energy Plan (SSEP).

The impact of these “gateways” varies significantly across the technology mix:

-

Offshore Wind: As the “backbone” of the 2030 goal, offshore wind is largely prioritized, with the reform providing much-needed certainty for the massive 50 GW target. Most viable offshore projects will be fast-tracked into Gate 2 Phase 1 (pre-2030) to ensure they receive the grid infrastructure investment they require.

-

Onshore Wind: The impact is highly zonal. In Scotland, where the queue is oversubscribed, the gateways act as a strict culling mechanism, allowing only the most advanced projects to proceed. Conversely, in England and Wales, the reforms aim to “pull forward” ready projects to fill regional shortfalls.

-

Solar PV: Solar faces a “mixed bag” scenario. While thousands of megawatts have been cleared for 2030, the gateways impose strict zonal capacity caps. Solar projects in areas with high grid congestion may find themselves stuck in Gate 1 (indicative offers only) or pushed to Phase 2 (post-2030) if the local 2030 “need” is already met by more advanced projects.

-

Battery Energy Storage (BESS): BESS has seen the most dramatic “queue cleansing.” Because the previous queue was flooded with speculative battery applications (often many times the actual system requirement), the Gate 2 criteria have been used to deprioritize over 150 GW of storage. Only those strategically located to provide flexibility or co-located with generation are being prioritized, forcing a shift from standalone “zombie” projects to high-utility, ready-to-build assets.